Many business ventures generate tax losses, especially in the first few years of operation or under adverse conditions. When can losses be deducted — and how much can you deduct in any given year? This article explains new limitations on the ability of individual taxpayers to deduct losses from pass-through business entities, including sole proprietorships, limited liability companies (LLCs) treated as sole proprietorships for tax purposes, partnerships, LLCs treated as partnerships for tax purposes and S corporations.

Before the Tax Cuts and Jobs Act (TCJA), an individual taxpayer's business losses could usually be fully deducted in the tax year when they arose. That was the result unless:

Old Rules

- The passive loss rules or some other provision of tax law limited that favorable outcome, or

- The business loss was so large that it exceeded taxable income from other sources, creating a so-called "net operating loss" (NOL).

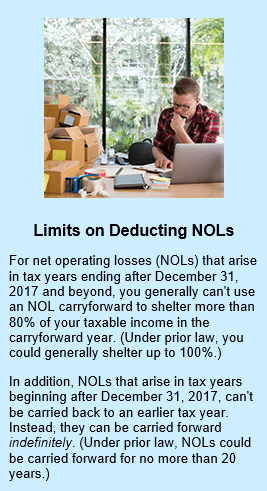

Under prior law, you could carry back an NOL to the two preceding tax years or carry it forward for up to 20 tax years.

Current Rules

For 2018 through 2025, the TCJA changes the rules for deducting an individual taxpayer's business losses. Unfortunately, the changes aren't favorable.

If your business or rental activity generates a tax loss, things get complicated. First, the passive activity loss (PAL) rules may apply if it's a rental operation or you don't actively participate in the activity. In general, the PAL rules only allow you to deduct passive losses to the extent you have passive income from other sources, such as positive income from other business or rental activities or gains from selling them.

Passive losses that can't be currently deducted are suspended. That is, they're carried forward to future years until you either have sufficient passive income or sell the activity that produced the losses.

To make matters worse, after you've successfully cleared the hurdles imposed by the PAL rules, the TCJA establishes another hurdle: For tax years beginning in 2018 through 2025, you can't deduct an "excess business loss" in the current year.

An excess business loss is the excess of your aggregate business deductions for the tax year over the sum of:

- Your aggregate business income and gains for the tax year, and

- $250,000 or $500,000 if you are a married joint-filer.

The excess business loss is carried over to the following tax year and can be deducted under the rules for net operating loss (NOL) carryforwards. (See "Limits on Deducting NOLs" at right.)

Important: This new loss deduction rule applies after applying the PAL rules. So, if the PAL rules disallow your business or rental activity loss, you don't get to the new loss limitation rule.

Real-World Examples

To illustrate how these new rules work, consider Ed, an unmarried individual who owns rental real estate. In 2018, he has a $300,000 allowable loss from his rental properties (after considering the PAL rules). So, his excess business loss for the year is $50,000 ($300,000 – the $250,000 excess business loss threshold for an unmarried taxpayer).

Ed has no other business or rental activities, but he has $400,000 of income from other sources. Ed can deduct the first $250,000 of his rental loss against his income from other sources.

The $50,000 excess business loss is carried forward to Ed's 2019 tax year and treated as an NOL carryfoward to that year. Under the TCJA's revised NOL rules for 2018 and beyond, Ed can use an NOL carryforward to shelter up to 80% of his taxable income in the carryforward year.

If Ed's rental property loss for 2018 is $250,000 or less, he won't have an excess business loss, because the loss is below the $250,000 excess business loss limitation threshold for an unmarried taxpayer. So, he wouldn't be affected by the new loss limitation rule.

Alternatively, consider Fern and Fernando, a married joint-filing couple. In 2018, Fern has a $300,000 allowable loss from rental real estate properties (after considering the PAL rules).

Fernando runs a small startup business. He operates the business as a single-member limited liability company (LLC) that's treated as a sole proprietorship for tax purposes. For 2018, the business has a $100,000 loss.

Fern and Fernando have no other business or rental activities, but they have $550,000 of income from other sources. This couple doesn't have an excess business loss for the year, because their combined losses are $400,000, which is below the $500,000 excess business loss limitation threshold for a married joint-filing couple. So, they're unaffected by the new loss limitation rule. Therefore, they can use their $400,000 business loss to shelter income from other sources.

Practical Impact of New Loss Disallowance Rule

The rationale underlying the new loss limitation rule is to further restrict the ability of individual taxpayers to use current-year business losses (including losses from rental activities) to offset income from other sources, such as salary, self-employment income, interest, dividends and capital gains.

The practical impact is that your allowable current-year business losses can't offset more than $250,000 of income from such other sources or more than $500,000 for a married joint-filing couple.

The requirement that excess business losses must be carried forward as an NOL forces you to wait at least one year to get any tax benefit from those excess losses.

Rules for S Corporations, Partnerships and LLCs

For business losses passed through to individuals from S corporations, partnerships and LLCs that are treated as partnerships for tax purposes, the new excess business loss limitation rules apply at the owner level. In other words, each owner's allocable share of business income, gain, deduction or loss is passed through to the owner and reported on the owner's personal federal income tax return for the owner's tax year that includes the end of the entity's tax year.

To illustrate, consider Gerald and Gina, siblings who quit their jobs at the end of 2017 to start a flower shop. They operate the new business as an LLC that's treated as a 50/50 partnership for tax purposes. Gerald is single and Gina is a married joint-filer. They each invest $500,000 in the new enterprise.

The 2018 LLC tax return for the business reports a net loss of $700,000. Each owner is allocated a $350,000 loss. Neither owner has any income or losses from other business activities. But Gerald has $300,000 of income from a trust, and Gina's husband has $200,000 of salary income.

The excess business loss limitation rule is applied at the owner level. So, Gerald has an excess business loss of $100,000 from the LLC ($350,000 – the $250,000 excess business loss threshold for an unmarried taxpayer). For 2018, he can deduct $250,000 of the LLC loss (the amount up to the threshold) against his trust income. The $100,000 excess business loss is carried forward to his 2019 tax year as an NOL carryforward.

Gina, on the other hand, has no excess business loss from the LLC because her $350,000 loss is less than the $500,000 excess business loss limitation threshold for a married joint-filing taxpayer. For 2018, the first $200,000 of the LLC loss can be deducted against her husband's salary income. The remaining $150,000 loss from the LLC generates an NOL carryforward to her 2019 tax year.

Ask the Experts

There's a silver lining to the unfavorable loss rules: The new excess business loss limitation rules only apply to tax years beginning in 2018 through 2025, unless Congress decides to extend them. But, while they're around, the rules may cause some struggling business owners additional hardship when they can least afford it.

Are you expecting your business to generate a tax loss in 2018? If so, contact us to determine whether you'll be affected by the new loss limitation rules.

© Copyright 2018 Thomson Reuters

All rights reserved